What Issues Should I Consider When Reviewing My Existing Annuity?

Have you looked at your annuity lately? If you bought one years ago and haven't checked on it since, you might be missing out on better options or paying too much in fees. Just like you wouldn't drive your car for years without a tune-up, your annuity needs regular check-ups too.

Most people buy an annuity and then forget about it. But here's the thing: your life changes, the market changes, and better products come out all the time. What made sense five years ago might not be the best choice today.

This guide will walk you through 12 key areas to review when looking at your existing annuity. We'll keep things simple and focus on what really matters for your financial future.

Why Regular Annuity Reviews Matter

Think about it – when you bought your annuity, what was going on in your life? Maybe you were 55 and worried about market crashes. Now you're 62 and thinking more about income in retirement. Your needs have changed, so shouldn't your annuity strategy change too?

Here are the main reasons to review your annuity regularly:

- Market conditions change: Interest rates go up and down, affecting what new annuities offer

- Your life changes: Marriage, divorce, new kids, or health issues all impact your needs

- Better products emerge: Insurance companies create new features and better terms

- Fees add up: Small annual fees can eat away thousands over time

- Tax laws evolve: New rules might create opportunities or problems

Contract Fundamentals Review

1. Understanding Your Current Contract Terms

Let's start with the basics. Do you really know what you own? Many people have a general idea but haven't looked at the details in years.

Key things to check:

- What type of annuity do you have? Fixed, variable, or indexed?

- When did you buy it? This affects surrender charges and tax rules

- How much did you put in originally? Your "basis" for tax purposes

- What's it worth today? Both accumulation value and surrender value

- What interest rate are you getting? Guaranteed vs. current rates

Pro tip: Call your insurance company and ask for a current statement. Most companies also have online portals where you can check your account anytime.

2. Surrender Charge Schedule Analysis

Surrender charges are like early withdrawal penalties. They protect the insurance company's investment in selling you the annuity. But they also lock up your money.

Here's what to look for:

- How much would you pay to get out today? Usually a percentage of your account value

- When do these charges end? Most last 6-8 years from purchase

- Can you take some money without penalties? Many allow 10% withdrawals annually

Real example: Say you have $100,000 in an annuity bought three years ago with a 7% surrender charge that drops 1% each year. Today, you'd pay $4,000 to cash out completely ($100,000 × 4%). But you might be able to withdraw $10,000 with no penalty.

Performance and Value Assessment

3. Investment Performance Evaluation

How is your annuity actually performing? This depends on what type you have.

For fixed annuities: Compare your current interest rate to what new fixed annuities offer today. If new ones pay 2% more, that's a big difference over time.

For variable annuities: Look at how your investment options (sub-accounts) have performed compared to similar mutual funds or index funds.

For indexed annuities: Check your participation rate, cap rate, and any spreads. These determine how much market gains you actually get.

Simple performance check: Divide your current value by what you originally invested. Then divide by the number of years you've owned it. This gives you a rough annual return rate.

4. Fee Structure Comprehensive Analysis

Fees are the silent killer of annuity returns. They come in many forms and can add up quickly.

Common fees to check:

- Administrative fees: Usually $25-50 per year

- Mortality and expense charges: Often 1-1.5% annually for variable annuities

- Rider fees: Extra charges for income or death benefits, typically 0.5-1.5% per year

- Management fees: For variable annuity sub-accounts, usually 0.5-2% annually

- Surrender charges: We covered these above

Quick math: A variable annuity with 2.5% total annual fees costs you $2,500 per year on a $100,000 account. Over 20 years, that's $50,000 in fees!

5. Inflation Impact Assessment

Here's something most people don't think about: inflation slowly eats away at your money's buying power.

Let's say you have a fixed annuity paying 3% annually. Sounds good, right? But if inflation runs at 3% too, you're not really gaining any buying power.

Example: $50,000 today has the same buying power as about $37,000 did 10 years ago (assuming 3% inflation). Your annuity needs to grow faster than inflation to truly protect your wealth.

What to look for: Cost-of-living riders that increase your payments with inflation, or variable/indexed options that might outpace inflation over time.

Riders and Benefits Optimization

6. Current Rider Value Analysis

Riders are extra features you can add to annuities, usually for an additional fee. But are they still worth what you're paying?

Income riders: These guarantee you can withdraw a certain amount each year for life. Check if the guaranteed amount has grown and whether it still makes sense for your situation.

Death benefit riders: These protect your beneficiaries if you die before getting all your money back. But if your account has grown significantly, you might not need this protection anymore.

Long-term care riders: These increase payments if you need care. Compare the cost to standalone long-term care insurance – you might find better deals elsewhere.

7. Beneficiary Designation Review

When did you last update who gets your annuity when you die? Life changes, and so should your beneficiaries.

Check these details:

- Are your beneficiaries still alive and appropriate? Ex-spouses shouldn't usually be beneficiaries

- Do you have backup (contingent) beneficiaries? What if your primary beneficiary dies first?

- Are the percentages right? Maybe you want to split things differently now

- Do you need to update addresses or contact info?

Important note: Beneficiary forms override your will. So even if your will says something different, the annuity goes to whoever is listed on the beneficiary form.

Personal Situation Assessment

8. Life Changes Impact Evaluation

Your annuity should fit your current life, not your life from five years ago. Major changes might mean you need to adjust your strategy.

Key life events to consider:

- Marriage or divorce: This usually changes your income needs and beneficiary choices

- New children or grandchildren: You might want to provide for them

- Job changes: Different income levels affect how much guaranteed income you need

- Health issues: Might change your life expectancy planning

- Inheritance: Extra money might mean you need less guaranteed income

Question to ask yourself: If you were buying an annuity today with your current situation, would you buy the same one you have?

9. Current Financial Needs Analysis

Your financial needs probably aren't the same as when you first bought your annuity. Let's think about what you need now.

Consider these factors:

- How much liquid cash do you need? Annuities tie up money, so make sure you have enough accessible funds

- What are your retirement income goals? Do you need more guaranteed income or more growth potential?

- How's your risk tolerance? Maybe you're more conservative now, or perhaps you can handle more risk

- How does this annuity fit with your other investments? Good diversification means not putting all eggs in one basket

Market and Regulatory Considerations

10. Insurance Company Financial Strength Review

The insurance company backing your annuity needs to be financially strong. After all, they're promising to pay you for potentially decades.

Check these ratings:

- A.M. Best rating: A++ or A+ are top grades

- Standard & Poor's: AAA or AA are excellent

- Moody's: Aaa or Aa are the highest ratings

You can find these ratings online for free. If your company's ratings have dropped since you bought the annuity, that's a red flag.

What if ratings are poor? You might want to consider a 1035 exchange to move your money to a stronger company without tax penalties.

11. Regulatory and Tax Environment Changes

Tax laws and regulations change over time. What worked when you bought your annuity might not be optimal now.

Recent important changes:

- Required minimum distributions (RMDs): If your annuity is in an IRA, new rules might affect when you must start taking money out

- State regulations: Some states have changed their rules about annuity sales and consumer protections

- Federal tax changes: Tax rates and rules for retirement accounts evolve

Pro tip: The IRS allows Section 1035 exchanges that let you move from one annuity to another without immediate tax consequences. This can be useful if you find a better product.

Strategic Options and Next Steps

12. Optimization Strategies and Alternatives

After reviewing everything above, you have several options:

Keep your current annuity if:

- Performance is competitive with new options

- Fees are reasonable for what you get

- It still fits your current needs

- The insurance company is financially strong

Consider changes if:

- You're paying high fees for features you don't need

- Better products are available with similar or lower surrender charges

- Your needs have changed significantly

- The insurance company's financial strength has declined

Your main options:

- Do nothing: Sometimes the best choice is to keep what you have

- Make partial withdrawals: Take advantage of penalty-free withdrawal amounts

- 1035 exchange: Move to a better annuity without tax penalties

- Full surrender: Cash out completely (consider tax implications)

- Annuitize: Convert to guaranteed income payments

Review Frequency Recommendations

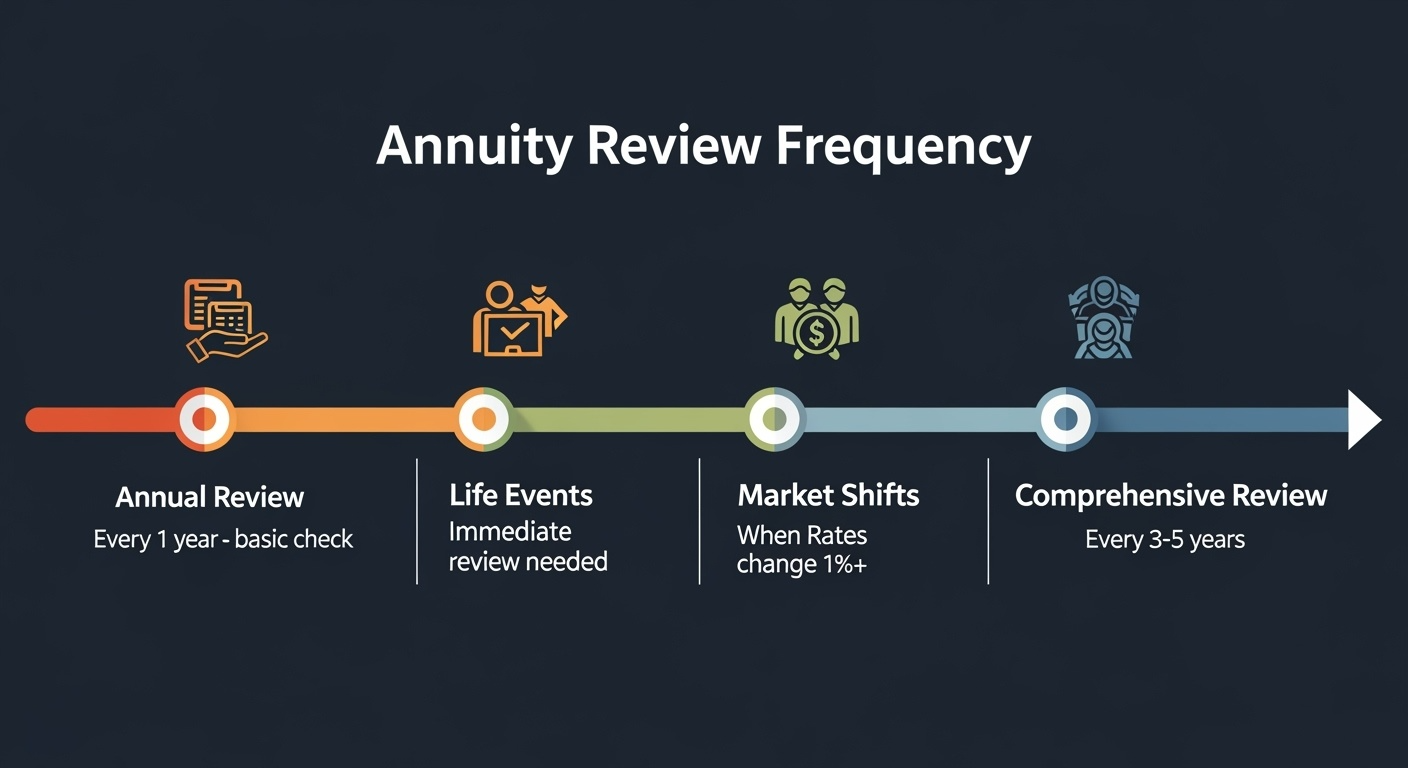

How often should you review your annuity? Here's a practical schedule:

Annual review: Check performance, fees, and basic account details every year.

Major life events: Review immediately after marriage, divorce, job changes, health issues, or inheritance.

Market shifts: When interest rates change significantly (up or down by 1% or more), it's time to look at alternatives.

Every 3-5 years: Do a comprehensive review like this guide suggests, especially as you approach or enter retirement.

Making Your Decision

Here's a simple framework for deciding what to do:

- Calculate total costs: Add up all annual fees and see what percentage of your account they represent

- Compare performance: How does your annuity compare to alternatives?

- Assess fit: Does it still match your current needs and goals?

- Consider surrender charges: Are they low enough that switching makes sense?

- Evaluate alternatives: Research what new products offer

Remember: The goal isn't to have the "perfect" annuity. It's to have one that fits your current situation at a reasonable cost.

Conclusion: Taking Action

Reviewing your annuity doesn't have to be complicated. The key is asking the right questions and being honest about whether your current annuity still serves you well.

Start with the basics: understand what you have, check the fees, and see how it's performing. Then think about whether it fits your current life situation.

If you discover problems or better alternatives, don't rush into changes. Take time to understand the tax implications and surrender charges. Consider talking to a fee-only financial advisor who can give you unbiased advice.

Most importantly, don't let your annuity run on autopilot forever. Your financial life is too important for that. Set a reminder to review it annually, and do a deep dive every few years.

Your future self will thank you for taking the time to make sure your annuity is working as hard for you as you worked to earn that money in the first place.

Action step: Schedule 30 minutes this week to gather your most recent annuity statement and work through the first few points in this guide. Small steps lead to big improvements over time.