Mortgage Free Retirement or Investment Income Which Path Is Better

As you approach or enjoy retirement, one big question becomes more urgent: Should you use extra money to pay off your mortgage or invest it for your retirement years? This decision takes on special importance when you're living on a fixed income or planning for that stage soon.

In 2025, the financial picture for retirees and pre-retirees is complex. Mortgage rates sit between 6.5% and 7% for new loans, but many approaching retirement still have older mortgages with rates below 5%. Meanwhile, safer investments like bonds and CDs now offer 4-5% returns – much better than the near-zero rates of a few years ago.

This creates an important question for those in their 50s, 60s, and beyond: Is it better to enter retirement debt-free with a paid-off home, or keep a low-rate mortgage and invest for additional income?

The answer depends on your unique situation. This guide will help you make this critical retirement decision by exploring eight key factors with a special focus on retirement needs and concerns.

The Financial Mathematics for Retirement Planning

The Basic Retirement Equation

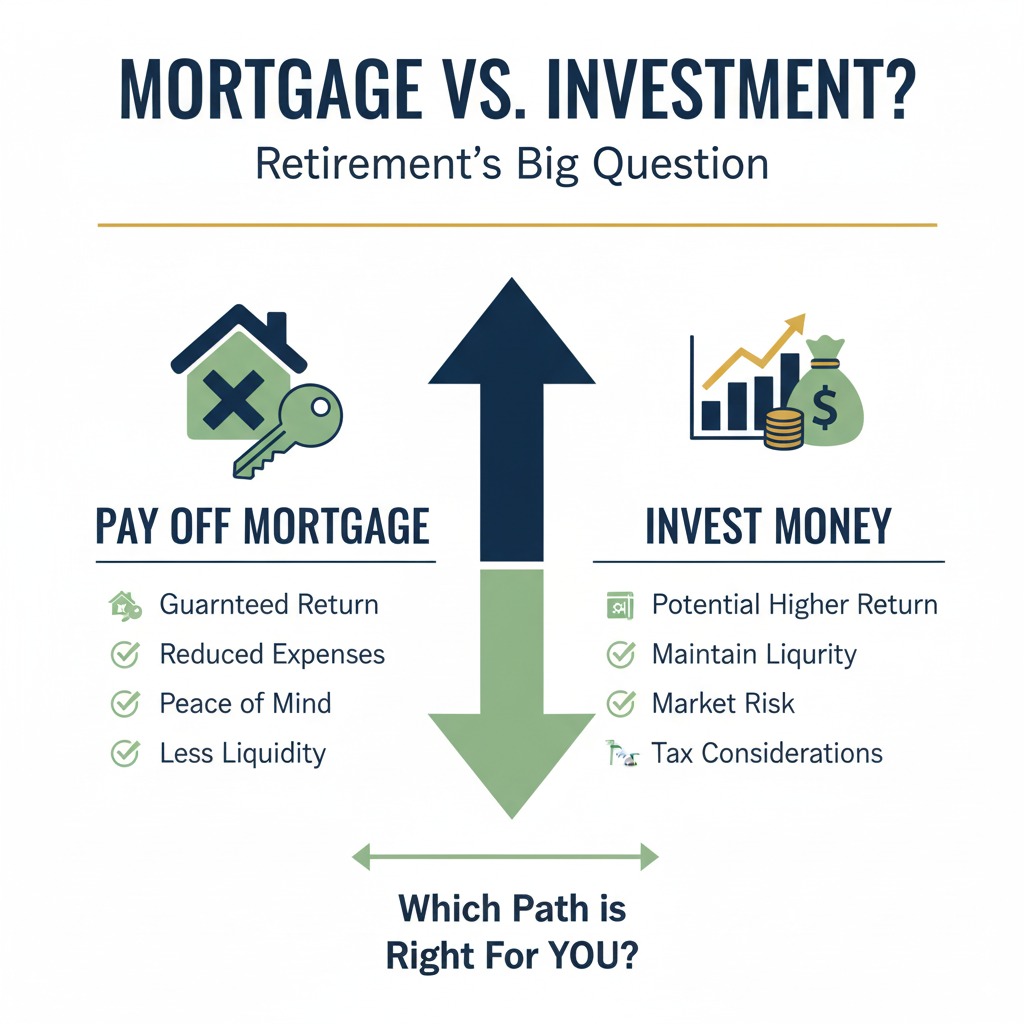

When considering this decision near or in retirement, you're essentially comparing:

- The guaranteed return from paying off your mortgage (your interest rate)

- The potential return from keeping those funds invested

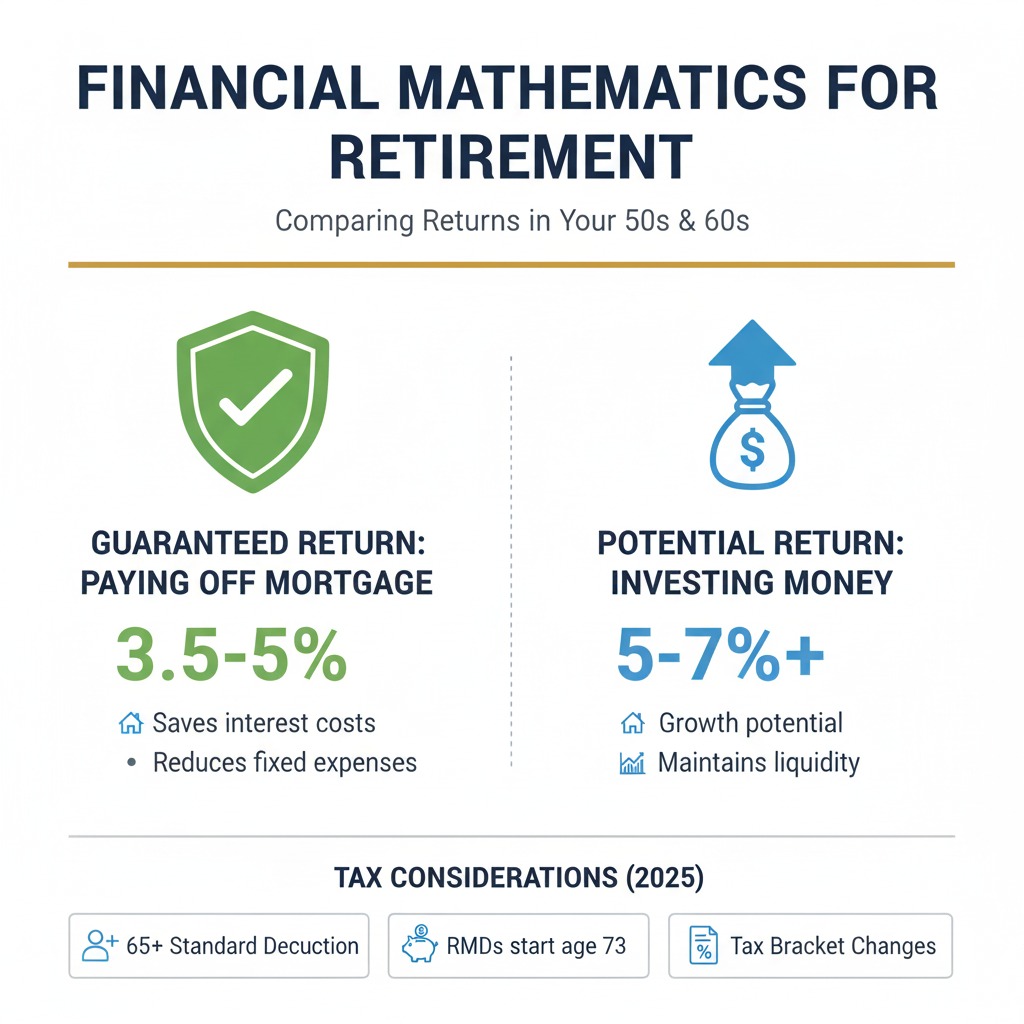

For example, if your mortgage rate is 4%, every extra dollar you pay saves you 4 cents in interest each year. But those same dollars might earn 5-7% in a conservative investment portfolio.

The math changes as you age. With fewer working years ahead, you have less time to recover from investment losses, making the guaranteed return from mortgage paydown more attractive than it might have been in your younger years.

Retirement-Focused Time Value of Money

In retirement planning, the time horizon shortens. A 65-year-old has a different perspective than a 35-year-old:

- Investment compounding has less time to work its magic

- The benefit of mortgage interest savings becomes more immediate

- Monthly cash flow becomes more important than long-term growth potential

Tax Considerations for Retirees

Retirement brings special tax situations:

- You may drop into a lower tax bracket when you stop working

- Required Minimum Distributions (RMDs) from traditional retirement accounts start at age 73

- The standard deduction is higher for those 65 and older ($16,550 for single filers and $32,400 for married filing jointly in 2025)

These factors can change the math on whether mortgage interest provides any tax benefit for you.

Retirement Scenario Example

Let's look at a common retirement scenario:

Scenario: 67-year-old couple with a $150,000 mortgage balance at 3.5% with 15 years remaining

Option 1: Pay off mortgage using $150,000 from investments

- Guaranteed "return": 3.5% (mortgage interest saved)

- Monthly payment eliminated: $1,075 (improved cash flow)

- Investments reduced by $150,000

- Keep the $150,000 invested at potential 5% return

- Continue making $1,075 monthly payments

- Maintain liquidity and potential for higher returns

- Accept the ongoing debt and monthly payment obligation

The difference might seem small (3.5% vs. 5%), but for retirees, the improved monthly cash flow and peace of mind from being debt-free often outweigh the potential for slightly higher investment returns.

Your Retirement Financial Foundation

Before deciding between mortgage paydown and investing, ensure your retirement foundation is secure.

Retirement Emergency Fund

In retirement, your emergency fund may need to be larger than the traditional 3-6 months of expenses. Many financial planners recommend retirees keep 1-2 years of expenses in cash or cash equivalents to protect against having to sell investments during market downturns.

This "retirement cash buffer" should be established before making extra mortgage payments.

Debt Profile in Retirement

Carrying debt into retirement creates additional risk:

- Fixed debt payments on a potentially fixed income

- Less flexibility to handle unexpected expenses

- Potential need to withdraw from retirement accounts to make payments

Most financial advisors recommend eliminating high-interest debt before retirement. Mortgage debt, with its typically lower interest rate and tax advantages, is usually the last debt to consider eliminating.

Liquidity Needs in Retirement

Access to Cash in Later Years

As you age, health expenses often increase. According to research from Fidelity's Retiree Health Care Cost Estimate, the average 65-year-old couple retiring in 2024 needed approximately $315,000 saved for healthcare expenses in retirement.

Keeping money invested rather than paying off your mortgage maintains access to these funds for potential healthcare needs or other emergencies.

Home Equity Options for Retirees

If you pay off your home, that equity isn't lost – it's just less accessible. Retirees have several ways to tap home equity if needed:

- Home equity line of credit (requires income qualification)

- Cash-out refinance (requires income qualification)

- Reverse mortgage (available to homeowners 62+)

- Downsizing to a less expensive home

Each option has pros and cons, but they all take time to arrange – something to consider when weighing liquidity needs.

Investment Return Potential for Retirees

Age-Appropriate Investment Options

Retirement portfolios typically shift toward more conservative allocations:

- More bonds and fixed income (4-5% yields in 2025)

- Fewer stocks (with focus on dividend-paying stocks)

- Alternative income investments (annuities, REITs)

These lower-risk investments may yield less than aggressive growth portfolios, narrowing the gap between investment returns and mortgage interest rates.

Sequence of Returns Risk

One of the biggest risks for retirees is "sequence of returns risk" – the danger of market downturns early in retirement when you're beginning to withdraw from investments.

Paying off your mortgage reduces this risk by:

- Lowering your monthly expenses (reducing the amount you need to withdraw)

- Decreasing your exposure to market volatility

- Providing a guaranteed "return" (interest saved) regardless of market performance

A study from the Journal of Financial Planning found that retirees with no mortgage were better able to weather market downturns without depleting their retirement savings.

Life Stage Considerations for Retirement

Pre-Retirement Decisions (Ages 55-65)

The years just before retirement are critical for this decision:

- You likely have peak earning years to put toward either mortgage or investments

- Retirement date becomes more concrete for planning purposes

- Risk tolerance often decreases as retirement approaches

Many pre-retirees accelerate mortgage payments during these years, aiming to enter retirement debt-free.

Early Retirement Phase (Ages 65-75)

During early retirement, consider:

- Your expected retirement lifestyle and travel plans

- Whether downsizing makes sense

- How Social Security claiming decisions affect your income

- Whether your mortgage extends well into your retirement years

If your mortgage will be paid off within 5 years of retirement anyway, accelerating payments may make less sense than keeping funds invested.

Later Retirement Phase (Age 75+)

In later retirement:

- Healthcare and long-term care costs often increase

- Managing a complex financial portfolio may become more challenging

- Home accessibility and maintenance concerns may arise

- Fixed monthly expenses become more burdensome

Being mortgage-free in this phase provides significant peace of mind and budget flexibility.

Tax Implications for Retirees

Retirement-Specific Tax Considerations

Retirees face unique tax situations:

- RMDs from tax-deferred accounts can push you into higher tax brackets

- Medicare premiums increase at certain income thresholds (IRMAA)

- Social Security benefits may be partially taxable based on income

Paying off a mortgage doesn't eliminate property taxes or the standard costs of home ownership, but it does remove one potentially tax-deductible expense.

Tax Diversification in Retirement

Having different types of accounts with different tax treatments provides flexibility in retirement:

- Tax-free accounts (Roth IRAs)

- Tax-deferred accounts (Traditional IRAs, 401(k)s)

- Taxable investment accounts

- Home equity

This diversification allows you to manage your tax bracket in retirement. Paying off your mortgage might make sense if it allows you to keep more money in tax-advantaged accounts longer.

Additional Carrying Costs for Retirees

Fixed Expenses in Retirement

Even after your mortgage is paid off, homeownership includes ongoing costs:

- Property taxes

- Homeowners insurance

- Maintenance and repairs

- Utilities

- Possibly HOA fees

For retirees on fixed incomes, these costs will continue to rise with inflation. When deciding whether to pay off your mortgage, remember that these other housing costs will remain.

Home Adaptation Needs

As you age, your home may need modifications for comfort and accessibility:

- Bathroom grab bars and walk-in showers

- Ramps or stair lifts

- Wider doorways

- First-floor bedrooms

Having funds available for these modifications (rather than tied up in mortgage paydown) could be important in later years.

Refinancing Considerations for Near-Retirees

Late-Career Refinancing

If you're within 10 years of retirement, refinancing requires careful consideration:

- A new 30-year mortgage would extend well into retirement

- A 15-year mortgage might increase monthly payments but be paid off sooner

- Closing costs might not be recouped if you plan to move in retirement

Many financial advisors suggest avoiding new 30-year mortgages once you're within 10-15 years of retirement.

Downsizing as a Strategy

Instead of focusing solely on paying down your current mortgage or investing, consider if downsizing would serve your retirement needs better:

- Selling your current home to buy a less expensive one outright

- Reducing ongoing maintenance, utilities, and property tax costs

- Freeing up home equity for retirement income

- Moving to a home better suited for aging in place

This "third option" often proves ideal for many retirees, eliminating the mortgage while also improving cash position.

Psychological and Behavioral Factors for Retirees

Retirement Peace of Mind

The psychological benefit of being mortgage-free in retirement is significant:

- Reduced anxiety about making monthly payments

- Greater feeling of security on a fixed income

- Elimination of a major monthly expense

- Pride and satisfaction in full homeownership

These emotional benefits often outweigh strict mathematical calculations for retirees.

Sleep Factor in Retirement

Many financial advisors refer to the "sleep at night factor" – how well do you sleep knowing your financial situation? For many retirees:

- Being debt-free improves sleep quality

- Market volatility causes anxiety

- Monthly fixed expenses create stress

Studies consistently show that retirees without mortgages report higher levels of financial satisfaction and lower stress levels, regardless of their overall wealth.

Legacy Considerations

How you want to leave assets to heirs may influence this decision:

- Paid-off homes can be simpler for heirs to inherit

- Investment accounts may receive a "step-up" in basis at death, reducing capital gains taxes for heirs

- Some retirees place high value on leaving a home free and clear to children or grandchildren

Advanced Strategies for Retirement Mortgage Decisions

Partial Mortgage Reduction

Instead of fully paying off your mortgage or keeping it entirely, consider:

- Making extra payments to reduce the term to align with your retirement date

- Refinancing to a shorter term if interest rates allow

- Making one large payment to reduce principal and then continuing regular payments

This balanced approach can provide some benefits of both strategies.

Reverse Mortgage Considerations

For those 62 and older who want to stay in their homes but access equity:

- Home Equity Conversion Mortgages (HECMs) allow you to tap equity without monthly payments

- The loan is repaid when you sell the home, move out, or pass away

- You maintain ownership and responsibility for taxes, insurance, and maintenance

Reverse mortgages have improved in recent years but still carry significant costs and considerations.

Qualified Charitable Distributions (QCDs)

For charitably-inclined retirees over 70½:

- QCDs allow direct transfers from IRAs to qualified charities

- These transfers count toward RMDs but aren't included in taxable income

- Lower taxable income might make keeping a mortgage less beneficial from a tax perspective

Creating Your Retirement Mortgage Decision Plan

Retirement-Focused Decision Framework

Ask yourself these key questions:

- Will having a mortgage payment strain my retirement budget?

- How many years of retirement will overlap with mortgage payments?

- What is my mortgage interest rate compared to likely investment returns for my risk tolerance?

- Would I feel more secure in retirement without mortgage debt?

- Do I have adequate cash reserves separate from retirement accounts?

- Might I want to move or downsize in retirement?

Implementation Timeline for Near-Retirees

If you're approaching retirement:

- 10+ years before retirement: Balance extra mortgage payments with maximum retirement contributions

- 5-10 years before: Consider a more aggressive mortgage paydown if being debt-free in retirement is important to you

- 2-5 years before: Evaluate refinancing options that could align payoff with retirement date

- At retirement: Reassess based on actual retirement budget and income

Conclusion

The Retirement-Focused Decision

For those in or near retirement, this decision often weighs more heavily toward mortgage paydown than it might for younger people:

- Fixed incomes make fixed expenses more burdensome

- Shorter time horizons reduce investment compounding benefits

- Sequence of returns risk makes market volatility more threatening

- Peace of mind becomes increasingly valuable

Finding Your Retirement Balance

Most retirees benefit from:

- Having significant cash reserves for emergencies and opportunities

- Reducing or eliminating debt before or early in retirement

- Maintaining some investments for growth and inflation protection

- Simplifying their financial lives where possible

The right choice combines mathematical analysis with your personal comfort level and retirement goals. Whether you choose the security of a paid-off home or the potential growth of investments, make your decision based on what will help you enjoy a comfortable, confident retirement.

Remember that circumstances change, and so might your decision. Revisit your strategy periodically, especially after major life events or significant market shifts. Your retirement years should be as free from financial stress as possible, whatever path you choose.

👉 If you would like to get a FREE retirement assessment, click the link to schedule your 20-minute call to start the retirement assessment process