Eight Tax Strategies That Could Save Retirees Thousands Before Year-End

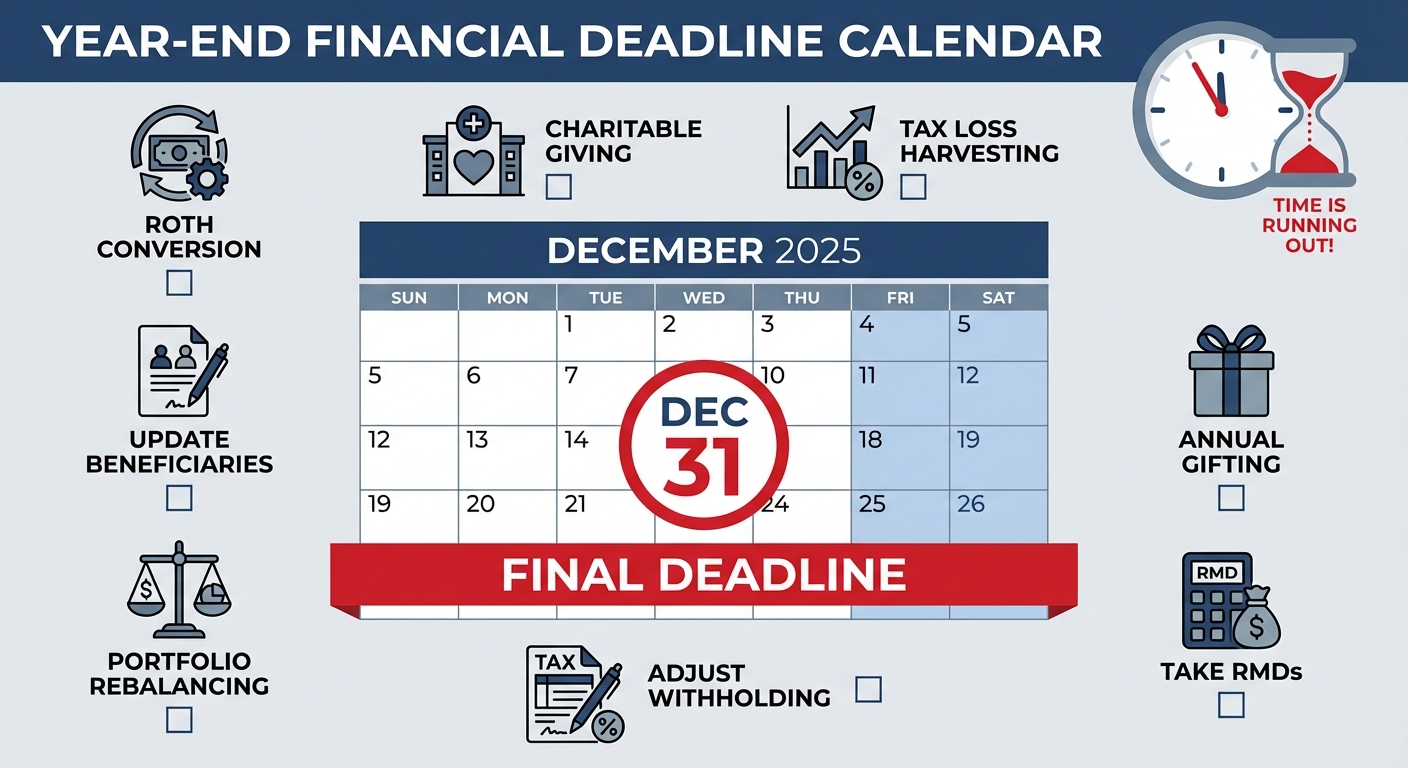

Time is running out. Every year, December 31st arrives faster than we expect, and once that date passes, your tax situation becomes permanent. No do-overs. No second chances. But right now, in these final weeks, you still have the power to make strategic decisions that could save you thousands of dollars.

The answer to reducing your tax burden as a retiree lies in taking specific actions before the calendar year closes. These eight strategic moves can dramatically lower your tax bill, reduce future mandatory withdrawals, and keep more of your hard-earned money working for you instead of going to the IRS.

The best part? You don't need to be a tax expert to implement them, but you do need to act quickly.

Key Takeaways

- Roth conversions let you pay taxes at today's lower rates and create tax-free income for life

- Qualified charitable distributions allow you to give to charity completely tax-free while satisfying required minimum distributions if you're over age 70½

- Tax loss harvesting offsets capital gains, while gain harvesting in the zero percent bracket (up to $96,700 taxable income for married couples) resets cost basis without paying taxes

- Charitable bunching concentrates multiple years of giving into one year to exceed the standard deduction threshold of $33,200 for married couples over 65

- RMD compliance is critical—missing the December 31st deadline costs 25 percent of the missed amount, and the RMD age is currently 73

- Year-end withholding from IRAs can eliminate underpayment penalties even if done in December because the IRS treats it as paid evenly throughout the year

- Strategic rebalancing and donating appreciated securities creates tax savings while maintaining your investment strategy

- Annual gifting of $19,000 per person reduces taxable estates without using lifetime exemptions, which are scheduled to sunset after 2025

- December 31st is an absolute deadline—you cannot make retroactive tax moves after the year closes

- These strategies work best when coordinated together as part of a comprehensive retirement tax plan with professional guidance

Why Year-End Tax Planning Matters in Retirement

Retirement changes everything about your tax situation. When you were working, taxes were straightforward, your employer withheld money from each paycheck. But retirement introduces complexity that catches many people off guard.

Now you're managing multiple income streams: Social Security benefits that may or may not be taxable, pension payments, required withdrawals from retirement accounts, investment income, and potentially part-time work. Each gets taxed differently, and their interactions can create unexpected tax situations.

Here's what surprises most retirees: your tax rate in retirement might actually be higher than during your working years if you don't plan carefully.

Required minimum distributions can push you into higher tax brackets, Medicare premiums can skyrocket based on your income, and Social Security benefits that could have been tax-free suddenly become taxable.

December represents your last opportunity each year to exercise control over these factors. Once January arrives, most of these strategies become unavailable until the following December.

Understanding Tax Brackets First

Before diving into specific strategies, understand one fundamental concept: tax brackets. This drives nearly every tax planning decision you'll make in retirement.

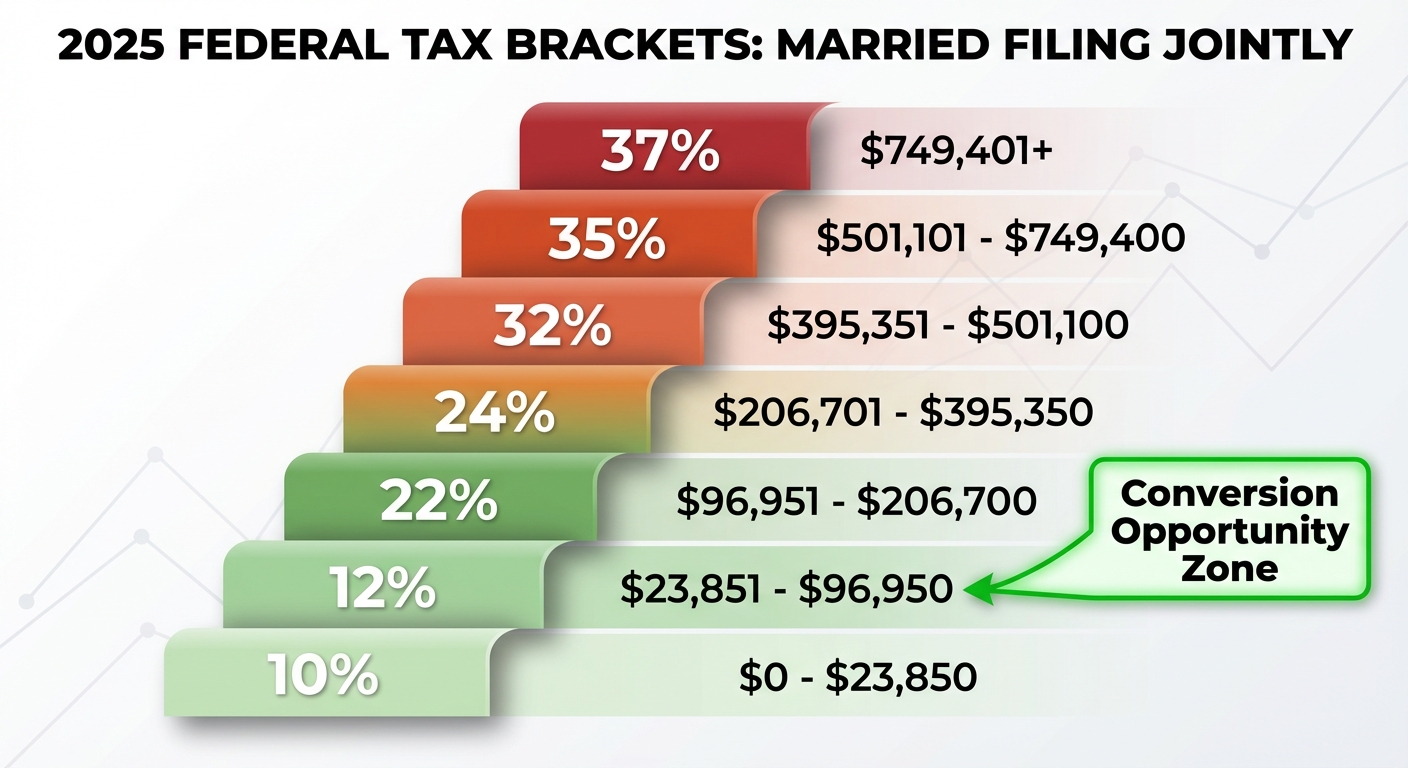

The United States uses a progressive tax system where different portions of your income get taxed at different rates. For 2025, if you're married filing jointly, the first portion of your taxable income up to $23,850 gets taxed at 10 percent. The next chunk up to $96,950 gets taxed at 12 percent. Then 22 percent, and so on.

Every dollar you keep in a lower bracket saves you real money. The difference between the 12 percent and 22 percent bracket is significant, that's an extra 10 cents on every dollar going to taxes.

Most retirees find themselves in the 12 percent or 22 percent bracket during their early retirement years. This creates a "tax opportunity window", a period when your income is lower than it will be later when required minimum distributions kick in at age 73.

Tax brackets are adjusted annually for inflation by the IRS. For the most current tax rates and brackets, you can review the official IRS tax rate tables to see exactly where your income falls and plan your conversions accordingly.

Strategy #1: Strategic Roth Conversions

A Roth conversion might be the single most powerful tax strategy available to retirees. You move money from a traditional IRA or 401(k) into a Roth IRA and pay taxes on the converted amount now. Once inside the Roth, it grows tax-free forever, and withdrawals are completely tax-free.

Why Convert Now

Converting now lets you fill up lower tax brackets at today's rates. It also reduces future required minimum distributions, which lowers taxes when you're in your 70s and 80s.

Here's a real example: You and your spouse are bringing in $80,000 of taxable income this year. The top of the 12 percent bracket for married couples in 2025 is $96,950. You have roughly $17,000 of room left in the 12 percent bracket.

If you convert $17,000 to a Roth IRA before December 31st, you'll pay 12 percent federal tax, about $2,040. If you wait until required distributions kick in and push you into the 22 percent bracket, that same $17,000 costs $3,740 in federal taxes. The difference? You just paid an extra $1,700 in taxes on the same money simply because you waited.

Additional Benefits

- Lower future RMDs: Smaller traditional IRA balances mean smaller required distributions later

- Reduced Social Security taxation: Less income means more of your Social Security stays tax-free

- Medicare premium savings: Lower income helps you avoid IRMAA surcharges

- Better inheritance: Your heirs receive tax-free accounts instead of inheriting your tax burden

Critical Timing

Roth conversions must be completed by December 31st to count for the current tax year. Under current law, tax rates are scheduled to expire after 2025. Starting in 2026, the 12 percent bracket could become 15 percent, and the 22 percent bracket could jump to 25 percent. This makes 2025 potentially the last year to lock in conversions at today's favorable rates.

Strategy #2: Qualified Charitable Distributions

If you're over age 70½ and give to charity regularly, qualified charitable distributions represent one of the most tax-efficient giving methods in the tax code.

How QCDs Work

You transfer money directly from your IRA to a qualified charity. The amount, up to $108,000 per person per year in 2025, counts toward your required minimum distribution but doesn't show up as taxable income on your tax return.

This is different from taking a distribution, paying taxes on it, and then writing a check to charity. With a QCD, the money never appears as income in the first place.

Why This Matters

- Lower taxable income: More of your Social Security might remain untaxable

- Medicare savings: Keeping income off your return helps avoid IRMAA surcharges

- Works without itemizing: You get the full benefit even with the standard deduction

Real-World Example

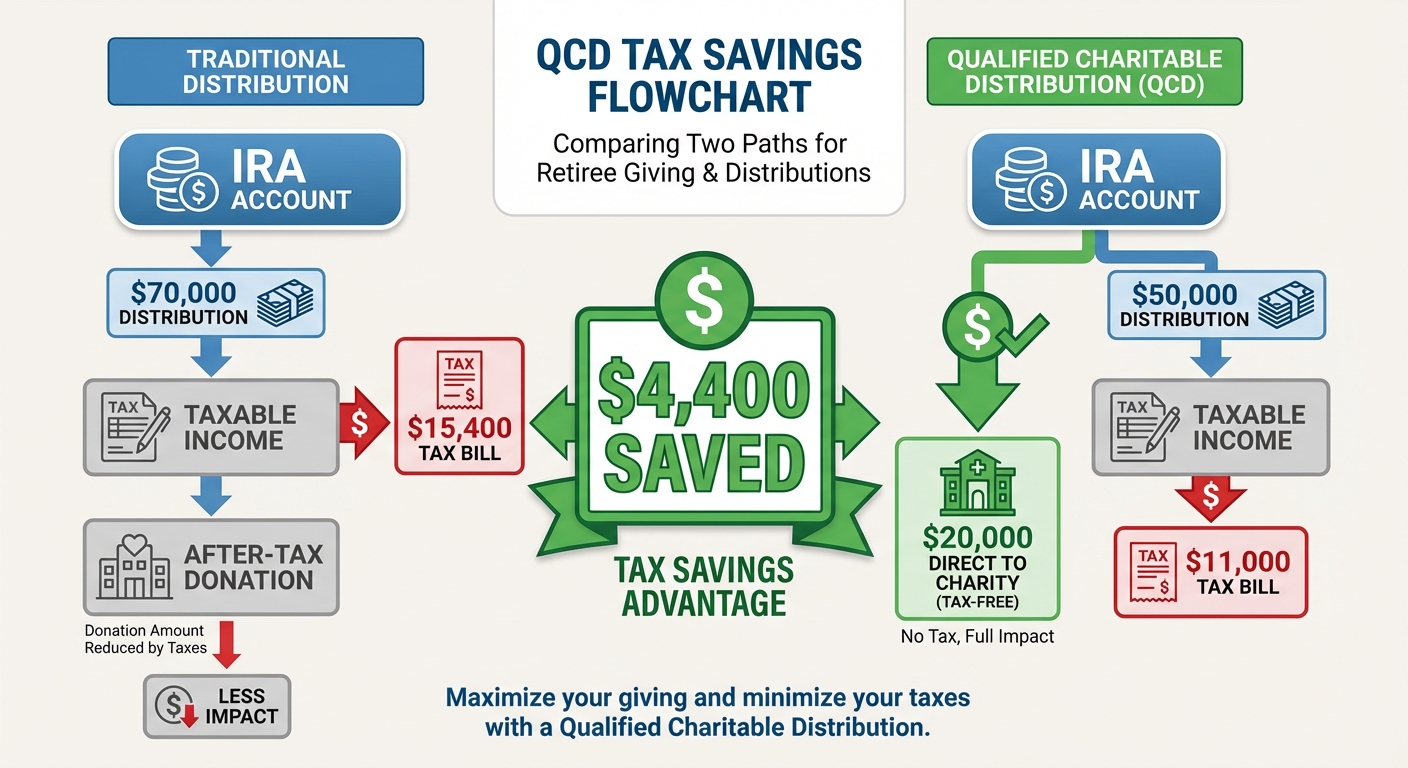

Your required minimum distribution is $70,000, but you only need $50,000 for living expenses. You typically give $20,000 annually to charity.

Without a QCD, you take the full $70,000 distribution and pay taxes on all of it. At the 22 percent bracket, that's $15,400 in federal taxes. You then write a $20,000 check to charity from after-tax money. If you take the standard deduction, that charitable gift doesn't reduce your taxes at all. Total tax bill: $15,400.

With a QCD, your IRA custodian transfers $20,000 directly to charities, and you take the remaining $50,000 as a regular distribution. You only pay taxes on $50,000, which comes to $11,000 at the 22 percent rate. You've saved $4,400 in federal taxes.

Important Details

- The transfer must go directly from your IRA custodian to the charity, you can't withdraw money and then write a personal check

- Request the QCD early enough in December to ensure processing before year-end

- The charity must receive and cash the check by December 31st

- Only works with IRAs, not 401(k)s or 403(b)s

- Charity must be a qualified 501(c)(3) organization

The rules surrounding qualified charitable distributions can be complex, especially regarding eligible charities and distribution timing. The IRS provides detailed guidance in Publication 590-B covering IRA distributions, which includes specific information about QCDs and how they interact with your required minimum distributions.

Strategy #3: Tax Loss and Gain Harvesting

Tax loss harvesting involves selling investments that have declined in value to generate losses that offset gains or income. But fewer retirees understand gain harvesting, which can be equally powerful.

Tax Loss Harvesting

If you have a taxable brokerage account, you can strategically sell investments that have lost value to create tax losses. These losses can offset any capital gains you've realized during the year. If losses exceed gains, you can use up to $3,000 of excess losses to offset ordinary income like pension payments or interest.

Example: Earlier this year, you sold stock for a $10,000 capital gain. If you find another investment that's down $10,000 from what you paid, you can sell it and the loss completely offsets the gain. Your net capital gain is zero, so you owe no capital gains tax.

Any losses beyond what you can use this year carry forward indefinitely to future years.

Gain Harvesting (The Hidden Opportunity)

If your taxable income is low enough, you can realize capital gains and pay zero federal tax on them. In 2025, married couples filing jointly with taxable income up to $96,700 pay zero percent on long-term capital gains and qualified dividends.

Let me emphasize: zero percent. Not a low rate. Zero.

Why This Works

You retired this year and won't start Social Security until next year. You're living off savings and maybe some part-time work that brings in $60,000 of income. After your standard deduction of $30,000 (or $33,200 if both spouses are over 65), your taxable income is around $27,000. You have nearly $70,000 of space in the zero percent capital gains bracket.

You could sell investments in your taxable account that have appreciated by up to $70,000 and pay absolutely no federal capital gains tax. Then immediately buy back the same investments if you want, this isn't a wash sale because you're recognizing a gain, not a loss.

You're resetting your cost basis to the current market value without paying any tax. Years later when your income is higher, you'll only owe taxes on growth from today's value forward, not from your original purchase price.

Advanced Strategy

Do Roth conversions to fill up your ordinary income tax brackets, then harvest capital gains to fill up the zero percent capital gains bracket. A married couple might convert $50,000 to a Roth IRA, staying in the 12 percent bracket (paying $6,000 in federal taxes), then harvest $60,000 in capital gains at zero percent tax.

They've created $110,000 of income but only paid $6,000 in taxes—an effective rate of about 5.5 percent.

Critical Rules

- Complete all transactions before December 31st

- Wash sale rule: Can't buy the same or substantially identical investment within 30 days before or after a loss sale

- Wash sales apply across all accounts, including IRAs and spouse's accounts

- Calculate taxable income carefully to ensure you're actually in the zero percent bracket

Strategy #4: Bunching Charitable Contributions

After the 2017 tax law changes, the standard deduction for married couples over 65 is $33,200 in 2025. For singles over 65, it's $17,000. This makes itemizing deductions difficult for most retirees.

How Bunching Works

Instead of giving the same amount to charity every year, bunch multiple years of donations into a single year. This creates a large enough charitable deduction to exceed the standard deduction threshold in that year. In following years, simply take the standard deduction again.

Example

You normally give $10,000 to charity every year. With only $10,000 in charitable contributions and maybe $5,000 in state taxes, you have $15,000 in potential itemized deductions. That's well below the $33,200 standard deduction, so you get no extra benefit from charitable giving.

Instead, give $30,000 all in one year. Now your itemized deductions jump to $35,000 the $30,000 in charitable contributions plus $5,000 in state taxes. That exceeds the standard deduction by about $1,800. If you're in the 22 percent bracket, that saves you about $396 in federal taxes.

Using Donor-Advised Funds

A donor-advised fund (DAF) solves the consistency problem. Contribute $30,000 to your DAF in year one and take the $30,000 deduction that year. Then over the next three years, direct the fund to grant $10,000 annually to your charities. From the charities' perspective, they're receiving their normal annual donation. From your tax perspective, you got the bunched deduction all upfront.

The money in a DAF can be invested and potentially grow, allowing you to give even more to charity over time.

Reality Check

Bunching is getting harder because the standard deduction keeps increasing. For many retirees, even bunching three or four years of contributions might not push itemized deductions high enough to make a meaningful difference. Run the actual numbers before committing to this strategy.

Strategy #5: Required Minimum Distribution Compliance

Once you reach age 73, you must start taking money from your traditional IRAs and 401(k)s whether you need it or not. Missing an RMD carries a 25 percent penalty on the amount you should have withdrawn.

Key RMD Rules

- Starting age: 73 under current law (increases to 75 in 2033)

- First-year exception: Can delay first RMD until April 1st of the following year, but this bunches two distributions into one tax year

- Deadline: December 31st each year (except first year)

- Multiple IRAs: Calculate RMD for each, but can take total from any one IRA

- 401(k)s: Must take RMD separately from each 401(k) account

- Roth IRAs: No RMDs during your lifetime

The SECURE 2.0 Act made significant changes to retirement account rules, including adjusting RMD ages and penalty structures. For a comprehensive overview of how these changes affect your retirement planning, visit the Department of Labor's retirement security resources or review Social Security's retirement planning tools to understand how RMDs coordinate with your Social Security benefits.

Year-End Withholding Strategy

If you realize in late December that you haven't withheld enough taxes for the year, you can catch up by requesting extra withholding from an IRA distribution. The IRS treats withholding from retirement distributions as if the tax was paid evenly throughout the year, even if you withhold it all in December.

If you're $10,000 short on tax payments, take a $10,000 distribution and withhold 99 percent for federal taxes. That $9,900 counts as if you paid it in equal installments all year, potentially eliminating underpayment penalties.

Review Beneficiaries Now

Year-end is the perfect time to review beneficiary designations on all retirement accounts. Your beneficiary designation supersedes your will. Outdated beneficiary forms create problems for heirs.

Update beneficiaries if you've experienced marriage, divorce, new grandchildren, or changed wishes. This simple 15-minute task prevents family disputes and ensures your money goes where you want it to go.

Strategy #6: Withholding and Estimated Tax Review

One of the biggest surprises for new retirees is getting hit with a large tax bill in April because they didn't have enough withheld during the year.

Safe Harbor Rules

Two ways to avoid underpayment penalties:

- Pay at least 90 percent of your current year's tax liability through withholding and estimated payments

- Pay at least 100 percent of your previous year's total tax (110 percent if income exceeded $150,000)

Most retirees find the second rule easier. Look at last year's tax return, find your total tax liability, and make sure you've paid at least that much this year.

Common Withholding Gaps

- Social Security: Typically withholds zero unless you specifically request it

- Investment income: Interest, dividends, and capital gains have no automatic withholding

- Rental income: No withholding

- Part-time work: May not withhold enough

Don't Forget State Taxes

Many states have their own income taxes with different withholding requirements. If you moved from a high-tax state to a low-tax or no-tax state during retirement, you might still owe taxes to your former state for income earned while you lived there.

Snowbirds who spend significant time in multiple states need to be careful about domicile rules. States want to claim you as a resident so they can tax your worldwide income. Have clear documentation of which state is your true domicile.

Strategy #7: Strategic Portfolio Rebalancing

Year-end is a natural time to rebalance your portfolio, and rebalancing creates tax planning opportunities when done thoughtfully.

Tax-Smart Rebalancing

Inside tax-deferred accounts like traditional IRAs and 401(k)s, rebalance freely without worrying about tax consequences. Selling appreciated stocks and buying bonds doesn't trigger taxable events inside these accounts.

In taxable brokerage accounts, every sale potentially triggers taxes. This requires strategic thinking.

Tax-Efficient Asset Location

- Taxable accounts: Hold index funds, ETFs, and stocks you'll hold long-term, these generate fewer taxable events

- Tax-deferred accounts: Hold bonds, actively managed funds, and REITs, assets that generate lots of taxable income

- Roth accounts: Hold your highest-growth potential investments, all growth is tax-free

Donating Appreciated Securities

If you hold stock or mutual fund shares that have appreciated significantly and you're planning to give to charity, donate the shares directly instead of selling them and donating cash.

When you donate appreciated securities held longer than one year, you get a charitable deduction for the full current market value and never pay capital gains tax on the appreciation. The charity receives the full value tax-free.

Example

You bought stock for $10,000 years ago, now worth $30,000. If you sold it, you'd owe capital gains tax on the $20,000 gain, potentially $3,000 to $4,000 depending on your bracket and state taxes.

If you donate the shares directly to charity, you get a $30,000 charitable deduction and avoid the capital gains tax entirely. The charity can sell the shares immediately and use the full $30,000. You've saved thousands in taxes while giving the same amount to charity.

Strategy #8: Strategic Gifting for High-Net-Worth Retirees

If you might face estate taxes, maximize your annual gifts to reduce your taxable estate.

Annual Gift Exclusion

You can give $19,000 to any person in 2025 without it counting toward your lifetime exemption. There's no limit on the number of people you can give to you could give $19,000 to each of your three children and five grandchildren, gifting $152,000 total in one year with no gift tax consequences.

Educational and Medical Exclusions

You can pay unlimited amounts for someone's tuition or medical expenses without it counting as a gift, as long as you pay directly to the educational institution or medical provider.

If you have grandchildren in college, this is a powerful way to reduce their financial burden while reducing your taxable estate.

Urgency for High Earners

The current estate tax exemption is around $13.99 million per person in 2025 (roughly $28 million per married couple). This exemption is scheduled to sunset after 2025, potentially dropping to around $7 million per person (inflation-adjusted) in 2026.

High-net-worth individuals should work with estate planning attorneys to maximize gifting strategies before the exemption potentially decreases.

Taking Action Before December 31st

These eight strategies work best when implemented as part of a comprehensive plan. Year-end tax planning isn't just about saving money this year, it's about setting yourself up so you're not paying more than necessary over the rest of your retirement.

Prioritized Action Steps

High Priority (Do First)

- Verify RMD compliance to avoid 25 percent penalty

- Review tax withholding to avoid underpayment penalties

- Check beneficiary designations to prevent estate issues

Significant Tax Savings

- Model Roth conversions, especially urgent given 2025 tax rate sunset

- Implement QCDs if charitably inclined and over 70½

- Harvest tax losses or gains in taxable accounts

Situational Strategies

- Charitable bunching (only if you can exceed standard deduction)

- Strategic gifting (primarily for high-net-worth estates)

Work With Professionals

These strategies should be implemented with personalized tax modeling. Everyone's situation differs based on income sources, account balances, state of residence, and personal goals.

To find qualified professionals in your area, consider using resources like the National Association of Personal Financial Advisors directory or the AICPA's CPA directory to locate fee-only financial planners or CPAs with retirement tax expertise who can coordinate these moves with your overall retirement income plan.

Ready to Take Control of Your Retirement Taxes?

The clock is ticking December 31st will be here fast. These eight strategies can save you thousands in taxes this year and potentially tens of thousands throughout retirement, but only if you act before year-end.

The retirees who thrive financially are the ones who plan proactively. You’ve worked hard to build your savings don’t let unnecessary taxes erode it.

If you’re ready to create a personalized retirement tax plan, click jhere to get a FREE retirement assessment, click the link to schedule your 20-minute call to start the retirement assessment process.